The Lion's Den Vol. 2 - Activists At The Gate

Why I expect a lot more activism around public tech companies

Hi everyone,

Thanks for the great responses to my last post. I’m encouraged to continue :)

I believe conditions are ripe for more activist campaigns and I expect to see more in the coming months. I’ll walk through why, what companies have a bullseye on their backs and what they can do about it in this ~5 min. read - Let’s go!

Uncertainty, Volatility & Bad Corporate Decisions = What Activists Look for

We’re in a uniquely uncertain environment. For the first time in 4 decades, the US is nearing double-digit inflation and there are real concerns about a recession. In the short term, if decisions around advertising budgets, new software implementation and other large projects get delayed, we’re going to see multiple companies posting disappointing outlooks for 2H’22 or missing earnings. Stress levels are already high with VIX hovering around 30, but while fear and greed have always moved the public market pendulum it feels like the swings in ‘22 have been sharper with multiple tech companies losing 30-40% a day(!) on disappointing earnings. Sometimes not even theirs. On top of this volatile environment, some companies are just making bad decisions and are inevitably “inviting” unwanted attention.

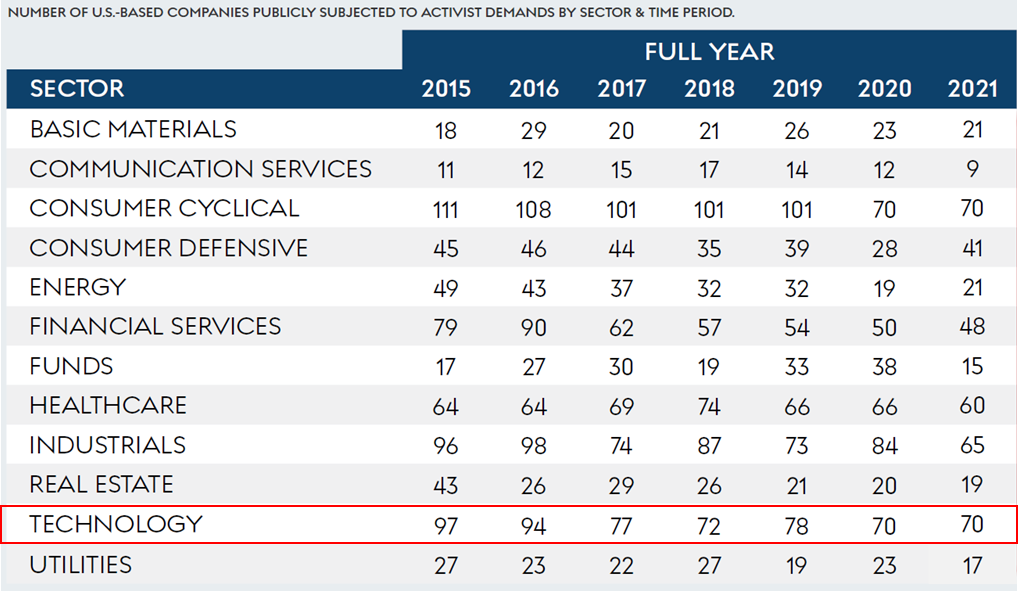

2020 and 2021 were good years for tech equity investors. Everything seemed to be up and to the right after the initial COVID shock and, as a result, we’ve seen ~20% less activist campaigns compared to 2015-2019. Now that there’s blood in the water, sharks will likely follow.

What Type of Companies Will Attract Activist Attention?

“Dream” companies - Simply put, too many companies that shouldn’t have gone public, did so. According to StockAnalysis, there were 1,035 IPOs on the US stock market in 2021, an all-time record. To put that in context, that figure was 2.2x higher than the 480 IPOs in 2020, which was also a record. Although quite a few of these IPOs were SPACs that will eventually disappear, many were regular way IPO/direct listings (and SPACs did push through >180 business combinations in 2021 alone, many of which in tech). I believe activists will look for companies with BIG promises and SMALL numbers. Many of these companies are either too early or not good enough to be public. This means they’ll systematically miss earnings, their technology might be promising, but not yet proven at scale and their internal infrastructure is likely weak. In some cases, these companies have cash balances that eclipse their market cap, implying the business is worth…nothing. I expect activists to demand a sale to a more established player or a merger with another startup in the space. In extreme cases, activists might even demand the company distribute its cash and shut down (especially if cash burn continues and cash>market cap for a prolonged period).

SMID Cap tech companies struggling to transition from growth to value - this is the category I find most interesting. Most tech companies that went public in the past decade sold investors on a growth story. Their industry was inefficient, they came up with a genius solution to fix it, have experienced rapid growth and, once at scale, they will generate a profit sometime in the long term (the concept of long-term margins is quite flexible - when I worked on IPOs and would ask my clients “when is long-term”, answers would range from 18 months to 10 years). For some companies, this path panned out. They were able to sustain growth, improve margins and crack the $10B market cap and are therefore less susceptible to activism barring a defining event (e.g. Zendesk’s strange attempt to buy Momentive, which angered shareholders and resulted in Zendesk’s take-private). However, for other companies growth has stalled for a variety of reasons while the cost structure and general mindset remained that of a fast-growing business. I find that these companies often have a hard time embracing the new reality. Instead, they:

Maintain a “fat” org structure with too many side-projects, hoping one will reignite growth.

Look for game-changing acquisitions for which they often overpay in order to “buy another leg of growth”.

Announce ill-advised share buybacks. I’ve yet to see an analysis proving that small companies with limited balance sheets and profits can systematically create value with episodic buybacks. I have, however, seen plenty of data showing that such decisions often lead to overpaying, throwing money away and not really moving the stock.

I consider all of these as an “open invitation”. I believe activists will look for companies with $1-10B market cap that used to grow 30-50% but have slowed down without meaningfully improving profitability. Activists will demand cost cutting, focusing on core offerings or exploring a sale and will likely look to reshuffle the board.

Peers with meaningful valuation arbitrage - when companies trade at significant discounts to their close peers they draw (sometimes unwarranted) attention. Even good companies can attract agitators that mostly look to…well, agitate. Activists may make all kinds of public claims/asks to improve the sentiment around the stock (e.g. demanding that the company buy/shed assets, focus/defocus on certain areas, align P&L/strategy with the more valuable peer, etc.). This is a “rock the boat” type strategy and I expect activists to hone in on companies with close peers exhibiting meaningful valuation gaps (e.g. companies in the “dev ops stratosphere” trading at relative discounts).

Potential “Shark Repellents”

All is not doomed. Activists prefer a “sure thing” and will usually avoid a prolonged campaign or a situation they’ll have a hard time getting out of. There are numerous factors that could deter activists from ever engaging. For example:

Dual class shares / special voting rights - Public/IPO investors don’t like these but have continuously relented so quite a few companies (~1/3 of tech IPOs in the past decade) have these in place. It’s interesting to track these provisions over time as they often sunset after a certain milestone (e.g. 10 years from IPO, % holding below certain threshold), making these companies “fair game”. Blue chip companies sometime renew their provisions (Shopify just did), but many companies can’t.

Cap table “blocks” / board structure - If VCs continue to hold meaningful stakes post IPO they can publicly express their long-term support of management to deter agitators. In some instances, companies can also raise a PIPE from a PE firm they are happy to align with in order to dissuade any potential activist. Another type of deterrent can be things like a staggered board, which would make any change longer to implement (less prevalent these days, but still exists).

Float - Many of the IPOs from the past ~24 months were welcomed by distracted investors. The IPO market was so busy that while IPO transactions went through, many companies weren’t able to build enough of a float. Companies usually issue only 8-15% of their shares in an IPO, hoping to do a follow-on quickly thereafter at a higher price. For those companies that weren’t able to, the float is sometimes so minimal that it would take an activist 2-3 quarters to build a meaningful position, which poses market/timing risk and raises the question of how to sell out of the position.

How Can Companies Prepare

I’m pretty sure you and I don’t worry about an earthquake every single day, but we do make sure our houses are built on solid ground, we know where to go if something happens, etc. Similarly, management teams and boards shouldn’t spend their days thinking about potential activists. They should focus on generating value, keeping their house in order and having a plan should something come up.

Since activists are usually drawn to easy prey, companies should take a proactive, critical look in the mirror to assess where they are vulnerable and start addressing the “low-hanging fruit”, i.e. issues that are relatively easy to address and that are in their control. For example:

Are Your Board Members “Friends & Family”? The #1 demand by activist is removing/appointing personnel and often it has to do with lack of diversity (minorities, LGBT, etc.), experience (sorry Mr. seed investor sitting on the comp committee) and tenure (board members serving 8+ years jump at the screen as a governance weakness).

Does Your P&L Have Glaring Holes? CFOs should compare their P&L to those of their closest peers, figure out what the biggest differences are and determine whether their growth and cost structure decisions make sense and can be defended if questioned publicly.

Do You Know What Your Top Holders Think? CEOs/IR/CFOs should regularly speak with their top 20 holders, communicate management’s strategy and gauge investors’ temperature around the current plan, how they think about valuation, their thoughts about other companies doing M&A/buybacks.

In the past few years, abundance of cheap capital and investor FOMO have allowed for lax governance and bad corporate decisions. Active shareholders weeding those things out might not necessarily be a bad thing. This post reminded me of the Blood // Water song so until next time I’ll leave you with this chilling, yet appropriate, 1-liner: “If you listen more closely, there's a knock at your front door".

Onwards!

Omer

@omerutah14