The Lion's Den Vol. 7 - The "IPO Winter", No End In Sight

Why I expect at least another 9-12 months of near-zero new tech issuances and what will drive the market out of hibernation

The IPO market for tech companies is as sluggish as it has been since the ‘08-’09 financial crisis. On one hand, there are hundreds of private companies at scale that, under normal circumstances, would test the markets and try to go public. On the other hand, the markets are incredibly volatile, many investors are over-invested in tech, tens of billions of dollars are still tied up with zombie SPACs waiting to be returned or redeemed and the general sentiment towards tech companies has changed, requiring management teams to fundamentally alter their hiring plan, sales forecast and cash burn.

Ok, so what next? In this post I’ll share my perspective of where we are in the cycle right now, what drivers can jumpstart the IPO market again and what I believe private companies should aim for in the next 2-4 years.

Looking Back, ~24 Months of Madness Needed a Reckoning

If you think about what the world (and by derivative, the small universe of technology companies) has experienced in the past 2 years, it’s almost hard to fathom. In the beginning of 2020, everything seemed to be going up and to the right for over a decade, then in March the entire world stopped and for a few weeks people were contemplating survival and existence. Then, just ~2 months later, the world of tech exploded with every acronym and tagline you can imagine catching fire: WFH, freelancers, ecommerce, virtual events, etc. Public investors, private investors, founders, consumers…we were all caught in the FOMO wave.

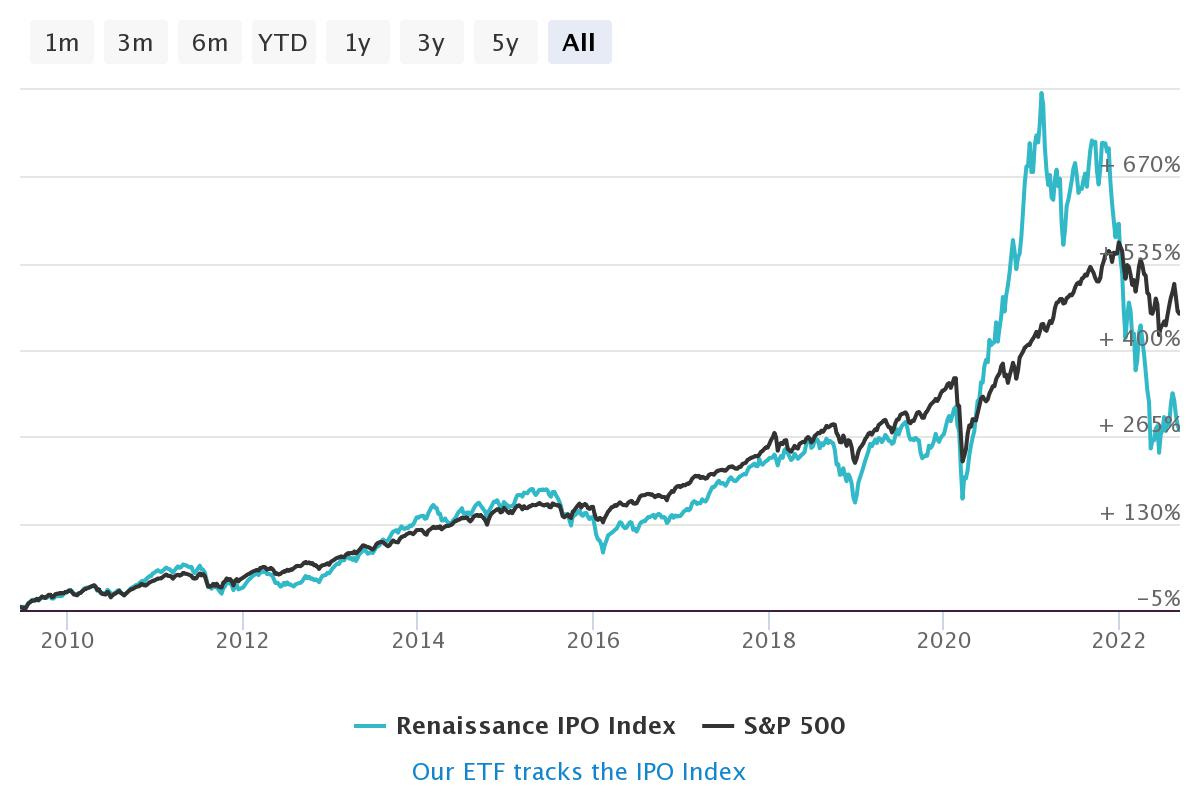

The IPO market during that 2-yr run saw unprecedented activity - hundreds of IPOs, hundreds of billions raised, SPACs with misaligned economics popping up everywhere and just like any overinflated balloon, at some point it had to pop. What we are seeing now in the tech market is a much needed reckoning that stems from a few main drivers, all intertwined:

Fundamental economic KPIs came to a halt. The reckless US government incentives stopped, new jobs weren’t being created as fast, supply chain challenges became a true bottleneck and the US found itself with a rapidly growing inflationary environment and limited ability to do something about it given the gigantic deficit.

Investors gradually came to realize that while COVID did accelerate macro trends such as digitization, adoption of ecommerce, remote work, etc., a lot of that was temporarily inflated as people were physically stuck at home, using every digital tool possible and buying everything online. The digitization trends are real and will continue, but the velocity of adoption misled investors to double-down on companies at prices that could not be justified with any economic reasoning.

Returns began normalizing again. During the “COVID wave”, investing in the IPO mini asset class yielded abnormal alpha above S&P return for no real reason other than exaggerated demand. When #1 and #2 above began materializing, investors cycled out of many tech IPOs they invested in, tilting the pendulum in the other direction.

This rollercoaster ride also had some unintended consequences that I find very interesting. Primarily, with so much supply of new issuances hitting the market investors have just become numb. There are dozens of recently IPOd companies with solid businesses, stable growth and good unit economics, but ZERO investor attention. These companies have little research coverage, almost no float and in some sense, you could argue many of the tech companies that went public in the past 24 months and have a market cap below $2B are quasi-private companies. This really matters for the recovery of the IPO market because VCs and founders now understand the bar is set higher and that in order to avoid that “no man’s land”, they have to wait longer and hit different milestones.

Looking Forward, The IPO Market Will Need a Jumpstart

In my experience, IPO activity is one of momentum, i.e. once the market opens up, it will return to normalized levels quickly because at the end of the day there are many private companies that are ready and there are hundreds of billions of dollars of institutional investors looking for alpha. In no specific order, here are a few key catalysts that could cause that jumpstart:

Economic recovery - may sound obvious, but still holds true. If inflation and interest rates stabilize, new jobs are created, etc. then we will see more enterprises accelerating big-budget digital transformation projects, more software tools adopted, more ecommerce activity and so forth. Not super optimistic about that one…

Big whale making a splash - very few private companies can successfully go public in any market. These are the most valuable private companies and when they do decide to go two things happen: first, investors pay close attention and try to get allocation. Second, when they don’t get enough or don’t get anything at all, they develop an appetite for the next best thing. If a company like Stripe decided to go, I could definitely see it being a very successful oversubscribed IPO that will open up a window for other companies.

SPAC liquidation - depending on the source you look at, it is estimated that ~$100B of investor capital is sitting on the sidelines in SPACs. These vehicles raised way too much capital and are on the clock. After a SPAC raises money in its IPO, it has 24 months to consummate a deal or return money to investors. Given that the highest ever SPAC IPO activity took place in Q4’20-Q1’21, we are going to see massive amounts of capital freed up by the end of Q1’23 and that capital will need to be deployed.

Sponsors’ patience - The volume of private growth and pre-IPO investments in the past 5 years has hit all-time highs year after year. It’s hard to imagine, but even the 2020 “harvest” will be 3 years old next year and sponsors are going to start looking for strategic alternatives. Some will go the M&A route, but I fully expect sponsors to push some of their companies to the public market as soon as practically possible.

My investment firm, Lion Investment Partners, focuses on late stage technology companies and when I speak to my portfolio CEOs, my advice is along these lines: First, there probably isn’t going to be an IPO market for at least another 9-12 months and I wouldn’t want to go first so the earliest CEOs should be thinking about is 2024. Until then, cash management is vital. Second, and in that vein, to attract investors you will need to choose a mid-term (i.e. 2-4 years) path: profitable growth OR uber-growth. If a company can consistently grow over 45-50% YoY with strong unit economics, burning cash is still the right decision. If not, management needs to start planning a transition to profitability quickly. Being a “tweener” with ~25-35% growth and near breakeven margins will put a company smack in what we used to (fondly) call at JPMorgan “The NOGASH Zone” (The No One Gives A Sh… Zone).

We are headed towards a super interesting 2023 as companies and their investors will need to internalize the reality of what is possible and contemplate which of the paths above is best for them.

Onwards!

Omer